DLH Holdings (DLHC)·Q1 2026 Earnings Summary

DLH Holdings Q1 FY26: EPS Beat on Smaller Loss as Small Business Transition Nears Completion

February 10, 2026 · by Fintool AI Agent

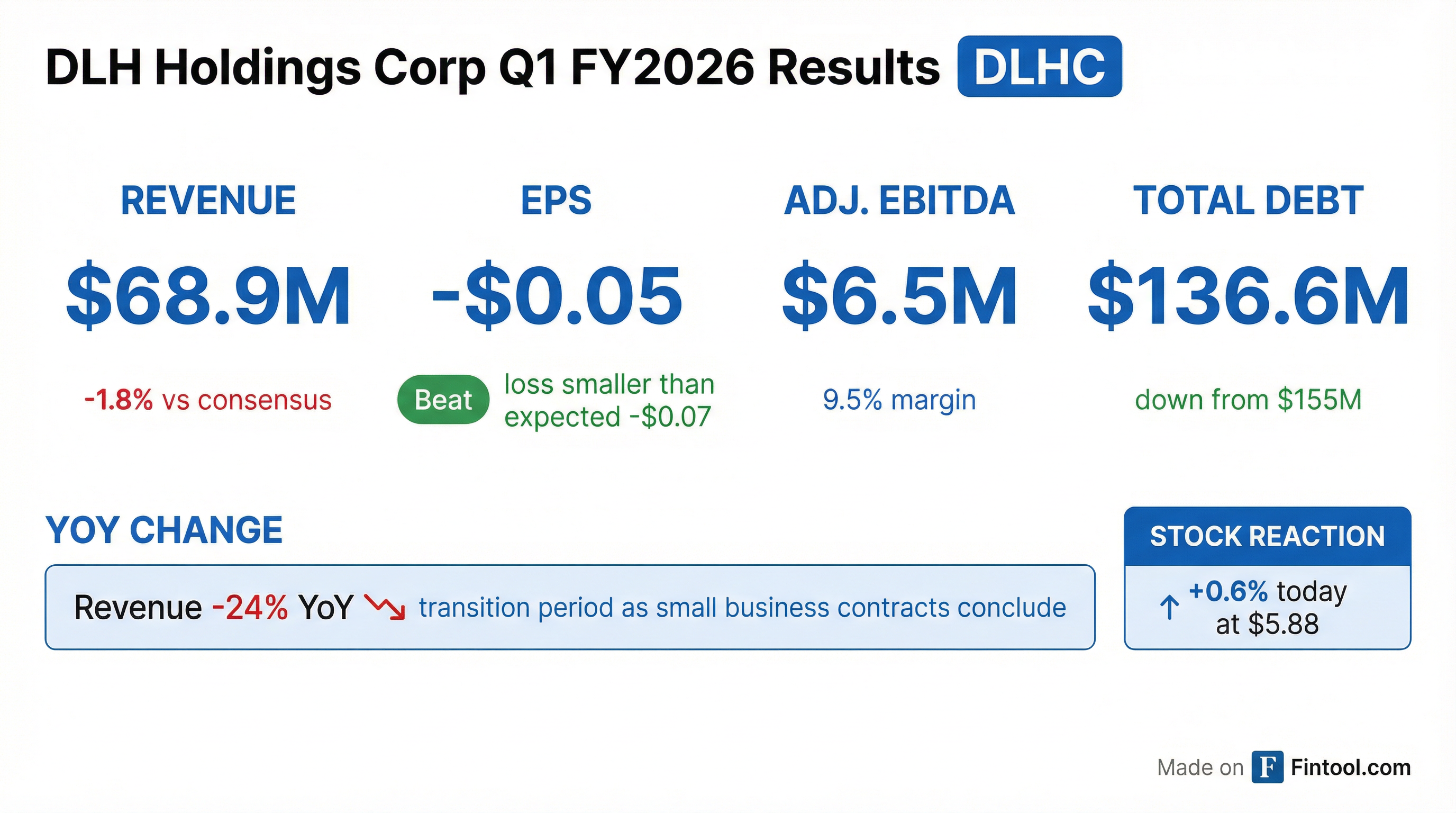

DLH Holdings (NASDAQ: DLHC) posted Q1 FY2026 results that beat EPS expectations while missing revenue consensus, as the government contractor continues working through its strategic transition away from small business set-aside contracts. The loss of -$0.05 per share was significantly better than the -$0.07 consensus, while revenue of $68.9M came in 1.8% below the $70.2M estimate.

Shares are up 0.6% to $5.88 in early trading as investors digest the mixed results and management's optimistic commentary on the improved federal funding environment.

Did DLH Holdings Beat Earnings?

Values retrieved from S&P Global and company filings.

The headline: DLH's loss was smaller than expected, driven by cost discipline even as revenue contracted sharply. The company beat EPS consensus by 23.7% (loss of -$0.05 vs expected -$0.07). However, the top line missed by 1.8% as the small business transition continues to weigh on revenue.

Context matters: Revenue declined 24% YoY but this was expected as DLH exits small business contracts. The key positive is that Adjusted EBITDA margin of 9.5% shows the company is successfully scaling down costs alongside revenue, though margin compressed from 11.0% in the year-ago quarter.

What Did Management Say About the Federal Funding Environment?

CEO Zach Parker struck an optimistic tone on the macro environment for federal contractors:

Improved funding clarity: "Fiscal 2026 budget appropriations provides clarity and stability for the balance of the fiscal year. Key Federal Health agencies received funding increases as compared to fiscal 2025 levels, reversing earlier projections of significant reductions."

Defense demand signals: Management highlighted that Defense & Intelligence customers are emphasizing rapid capability delivery, cost efficiency, and advanced technology integration—areas DLH cited as competitive strengths.

Federal Health priorities: The company sees opportunities in data modernization, interoperability, cybersecurity (Zero Trust), cloud migration, and AI adoption—positioning DLH for "modernization-driven awards."

Key takeaway: While near-term revenue is pressured by the small business transition, management believes the funding environment has improved materially and DLH is well-positioned for organic growth as it emerges from this transition period.

What Changed From Last Quarter?

Revenue decline accelerated from -3% sequential last quarter to -15% this quarter, though this includes seasonality effects and timing of contract transitions.

EBITDA margin improved despite lower revenue, reflecting successful cost management. The 9.5% margin is a sequential improvement from 8.1% in Q4 FY25, though still below the 11% levels from early FY25.

Debt ticked higher to $136.6M from $131.6M at fiscal year-end. Management attributed the increase to "prepayment of labor and payroll tax expenses timed around public holidays" and expects strong free cash flow to reduce debt by fiscal year-end.

How Is the Debt Situation Progressing?

DLH has been aggressively paying down debt from its 2021 acquisition spree. The trajectory remains positive despite the Q1 uptick:

Data from company filings.

Key debt commentary from management:

- "Remain well ahead of mandatory term repayment schedule with additional prepayments executed"

- "Compliant with all financial covenants as small-business transition is materially complete"

- "Expect to convert 50-55% of EBITDA earned during the fiscal year to debt reduction by the end of 4th quarter"

- "Collections accelerated in quarter 2nd half after resolution of government shutdown"

Bottom line: The Q1 debt increase is timing-related and management expects to resume debt paydown. If they convert 50-55% of EBITDA to debt reduction as guided, that implies $15-20M of debt paydown potential through end of FY26.

How Did the Stock React?

DLHC shares are trading up 0.6% to $5.88 in early trading—a muted reaction to the mixed results.

The stock has been range-bound between $5.50-$6.50 over the past several months as investors await signs that revenue has stabilized post-transition. Today's modest gain suggests the market views the results as roughly in-line with expectations, with the EPS beat offsetting the revenue miss.

Historical Beat/Miss Pattern

DLH has had a mixed track record vs. consensus estimates over the past two years:

Values retrieved from S&P Global.

Pattern: DLH has consistently missed revenue estimates during the small business transition period, but has shown better cost discipline with EPS results often beating or coming in-line with expectations.

Key Risks and Concerns

-

Revenue trajectory uncertainty: While management is optimistic about the funding environment, there's limited visibility on when revenue will stabilize and begin growing again.

-

Margin pressure: EBITDA margin has compressed from 11% to 8-9% over the past year. Cost cuts have helped but may have limits.

-

Debt levels: At $136.6M in debt against ~$85M market cap, DLH remains leveraged. Interest expense was $3.4M in Q1, eating into profitability.

-

Small cap illiquidity: With an $85M market cap and low daily volume, the stock can be volatile and difficult to trade in size.

-

Government budget risk: Despite improved appropriations, federal spending remains subject to political dynamics and potential future cuts.

Q&A Highlights: What Analysts Asked

CMOP Transition Timeline (Joe Gomes, Noble Capital)

Q: Where do the remaining CMOP contracts stand?

CFO Kathryn JohnBull confirmed DLH expects complete wrap-up of CMOP in Q3 FY26: "The cadence now that there seems to be a pretty manageable process for making those transitions, we are looking at probably a complete wrap-up of CMOP in Q3 of this current fiscal year."

CEO Zach Parker added: "We're really in the wind down phase across the board for the CMOP work. The VA has gotten a more, you know, a little battle rhythm set for being able to do some of the transitions."

Revenue Bridge Details

Q: What caused the $4M revenue shortfall beyond the $18M small business impact?

CFO JohnBull explained the remaining $4M was from "nicks and nibbles" of DOGE initiatives in early fiscal 2025 and the USAID international project that completed in January 2025. "A sundry of smaller impacts that were not strategic and not related to the small business set aside."

CIO-SP4 Cancellation Impact

The most significant pipeline update was the cancellation of CIO-SP4, a major contract vehicle DLH had anticipated using for organic growth:

CEO Parker: "CIO-SP4 has been canceled. And as we had stated before, we saw that as a very attractive and viable vehicle for us, with a number of opportunities that we had anticipated being able to bid in 2025."

Impact: Some opportunities shifted to vehicles where DLH cannot prime. However, CFO JohnBull noted: "The overwhelming majority of those opportunities appear headed places that we can and will compete as a prime."

Pipeline dryness: "We had one bid opportunity for the entire month of January, and, you know, that's just really, really trickling."

Shift Toward Commercial Best Practices

Management highlighted a significant trend in federal contracting:

CEO Parker: "We're seeing a major movement by a number of our customers, including Department of War, to leverage more commercial best practice vehicles and approaches... This administration is really, really keen to cut through those delays and to use more commercial best practices."

This shift toward Other Transaction Authorities (OTAs) means smaller initial pilot contracts before larger awards—a different revenue profile but potentially faster procurement cycles.

Cost Reduction Implementation

CEO Parker on cost actions: "We've implemented two major components of that indirect reduction. It's very important for us to maintain a competitive indirect cost profile to be able to compete organically."

CFO JohnBull on GAAP impact: "Both the impact of the reduction in cost as well as the cost of achieving those reductions is all reflected in the Q1 financials. And is also then considered as part of the crosswalk from standard EBITDA to adjusted EBITDA."

Commercial/Civilian Clarification (Bert Osterweis)

Q: Who are DLH's civilian clients? Can you expand into commercial work?

CEO Parker clarified that "civilian" refers to federal civilian agencies (NIH, CDC, DHS) rather than commercial clients. However, DLH does have a small biotech/biopharma commercial presence through university partnerships and grant-funded work. A new hire with FDA relationships may help expand this.

CFO JohnBull: "Those commercial enterprises need to access that government approval queue, and it's often an inscrutable protracted process for them, and so they're happy to opportunistically leverage our capability to help steer them through that."

Forward Catalysts

- CMOP wrap-up (Q3 FY26): Final transition completion removes key revenue headwind

- Contract win announcements: New awards would signal organic growth resuming

- Q2 FY26 results (May 2026): Evidence of revenue stabilization would be bullish

- Debt paydown progress: Continued deleveraging improves equity value

- Federal Health modernization awards: DLH is positioned for AI/cloud/cybersecurity contracts

- OTA/Commercial practice adoption: Faster procurement cycles could accelerate wins

This analysis was generated by Fintool AI Agent using data from company filings, S&P Global estimates, and market data. Last updated February 10, 2026.